Page 124 - HRC_AR2020

P. 124

122 I 2020 ANNUAL REPORT I financial reports

NOTES TO THE FINANCIAL STATEMENTS

FOR THE FINANCIAL YEAR ENDED 31 DECEMBER 2020 (CONTINuED)

19 DeriVatiVe financial assets/(liaBilities) (continued)

Derivatives designated as hedging instrument

(a) refining margin swap contracts

The Company purchases crude on an ongoing basis as the Company requires continuous supply of crude to produce

petroleum products. As a result of the volatility in crude price, the Company held refining margin swaps designated

as hedge of highly probable forecast crude purchases or firm commitments and sales of petroleum products to reduce

the volatility of cash flows.

The contracts are intended to hedge the volatility of the refining margin (differences between purchase price of crude

oil and sales price of petroleum products) for a period between 1 to 12 months (2019: 1 to 24 months). There was no

forecast transactions for which hedge accounting had previously been used, but which is no longer expected to occur.

The cash flow hedges of the highly probable forecast crude purchases or firm purchase commitments and

sales of petroleum products were assessed to be highly effective. The net unrealised gain of RM75,099,000

(2019: RM201,691,000), with a related deferred tax liability of RM18,024,000 (2019: RM48,406,000) was included

in other comprehensive income in respect of these contracts for the financial year. There is no ineffectiveness portion

of hedge accounting during the current and previous financial year.

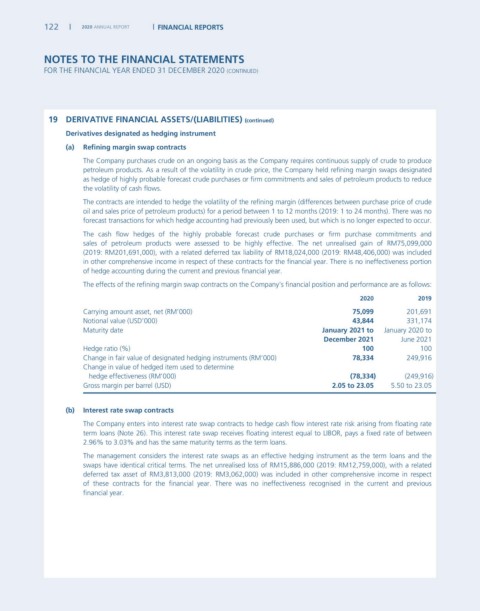

The effects of the refining margin swap contracts on the Company’s financial position and performance are as follows:

2020 2019

Carrying amount asset, net (RM’000) 75,099 201,691

Notional value (USD’000) 43,844 331,174

Maturity date January 2021 to January 2020 to

December 2021 June 2021

Hedge ratio (%) 100 100

Change in fair value of designated hedging instruments (RM’000) 78,334 249,916

Change in value of hedged item used to determine

hedge effectiveness (RM’000) (78,334) (249,916)

Gross margin per barrel (USD) 2.05 to 23.05 5.50 to 23.05

(b) interest rate swap contracts

The Company enters into interest rate swap contracts to hedge cash flow interest rate risk arising from floating rate

term loans (Note 26). This interest rate swap receives floating interest equal to LIBOR, pays a fixed rate of between

2.96% to 3.03% and has the same maturity terms as the term loans.

The management considers the interest rate swaps as an effective hedging instrument as the term loans and the

swaps have identical critical terms. The net unrealised loss of RM15,886,000 (2019: RM12,759,000), with a related

deferred tax asset of RM3,813,000 (2019: RM3,062,000) was included in other comprehensive income in respect

of these contracts for the financial year. There was no ineffectiveness recognised in the current and previous

financial year.