Page 125 - HRC_AR2020

P. 125

HENGYUAN REFINING COMPANY BERHAD I 123

19 DeriVatiVe financial assets/(liaBilities) (continued)

Derivatives designated as hedging instrument (continued)

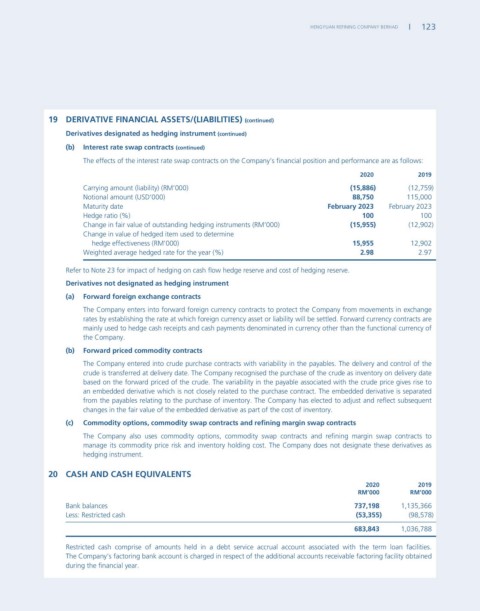

(b) interest rate swap contracts (continued)

The effects of the interest rate swap contracts on the Company’s financial position and performance are as follows:

2020 2019

Carrying amount (liability) (RM’000) (15,886) (12,759)

Notional amount (USD’000) 88,750 115,000

Maturity date february 2023 February 2023

Hedge ratio (%) 100 100

Change in fair value of outstanding hedging instruments (RM’000) (15,955) (12,902)

Change in value of hedged item used to determine

hedge effectiveness (RM’000) 15,955 12,902

Weighted average hedged rate for the year (%) 2.98 2.97

Refer to Note 23 for impact of hedging on cash flow hedge reserve and cost of hedging reserve.

Derivatives not designated as hedging instrument

(a) forward foreign exchange contracts

The Company enters into forward foreign currency contracts to protect the Company from movements in exchange

rates by establishing the rate at which foreign currency asset or liability will be settled. Forward currency contracts are

mainly used to hedge cash receipts and cash payments denominated in currency other than the functional currency of

the Company.

(b) forward priced commodity contracts

The Company entered into crude purchase contracts with variability in the payables. The delivery and control of the

crude is transferred at delivery date. The Company recognised the purchase of the crude as inventory on delivery date

based on the forward priced of the crude. The variability in the payable associated with the crude price gives rise to

an embedded derivative which is not closely related to the purchase contract. The embedded derivative is separated

from the payables relating to the purchase of inventory. The Company has elected to adjust and reflect subsequent

changes in the fair value of the embedded derivative as part of the cost of inventory.

(c) commodity options, commodity swap contracts and refining margin swap contracts

The Company also uses commodity options, commodity swap contracts and refining margin swap contracts to

manage its commodity price risk and inventory holding cost. The Company does not designate these derivatives as

hedging instrument.

20 casH anD casH eQUiValents

2020 2019

rM’000 rM’000

Bank balances 737,198 1,135,366

Less: Restricted cash (53,355) (98,578)

683,843 1,036,788

Restricted cash comprise of amounts held in a debt service accrual account associated with the term loan facilities.

The Company’s factoring bank account is charged in respect of the additional accounts receivable factoring facility obtained

during the financial year.