Page 106 - HRC_AR2020

P. 106

104 I 2020 ANNUAL REPORT I financial reports

NOTES TO THE FINANCIAL STATEMENTS

FOR THE FINANCIAL YEAR ENDED 31 DECEMBER 2020 (CONTINuED)

4 financial risK ManaGeMent oBJectiVes anD policies (continued)

(a) Market risk (continued)

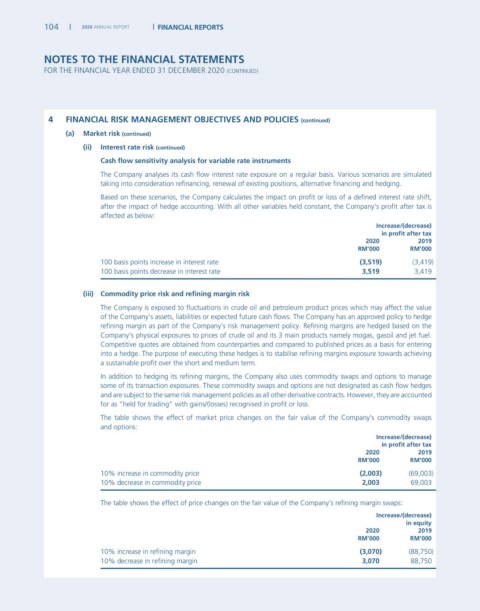

(ii) interest rate risk (continued)

cash flow sensitivity analysis for variable rate instruments

The Company analyses its cash flow interest rate exposure on a regular basis. Various scenarios are simulated

taking into consideration refinancing, renewal of existing positions, alternative financing and hedging.

Based on these scenarios, the Company calculates the impact on profit or loss of a defined interest rate shift,

after the impact of hedge accounting. With all other variables held constant, the Company’s profit after tax is

affected as below:

increase/(decrease)

in profit after tax

2020 2019

rM’000 rM’000

100 basis points increase in interest rate (3,519) (3,419)

100 basis points decrease in interest rate 3,519 3,419

(iii) commodity price risk and refining margin risk

The Company is exposed to fluctuations in crude oil and petroleum product prices which may affect the value

of the Company’s assets, liabilities or expected future cash flows. The Company has an approved policy to hedge

refining margin as part of the Company’s risk management policy. Refining margins are hedged based on the

Company’s physical exposures to prices of crude oil and its 3 main products namely mogas, gasoil and jet fuel.

Competitive quotes are obtained from counterparties and compared to published prices as a basis for entering

into a hedge. The purpose of executing these hedges is to stabilise refining margins exposure towards achieving

a sustainable profit over the short and medium term.

In addition to hedging its refining margins, the Company also uses commodity swaps and options to manage

some of its transaction exposures. These commodity swaps and options are not designated as cash flow hedges

and are subject to the same risk management policies as all other derivative contracts. However, they are accounted

for as “held for trading” with gains/(losses) recognised in profit or loss.

The table shows the effect of market price changes on the fair value of the Company’s commodity swaps

and options:

increase/(decrease)

in profit after tax

2020 2019

rM’000 rM’000

10% increase in commodity price (2,003) (69,003)

10% decrease in commodity price 2,003 69,003

The table shows the effect of price changes on the fair value of the Company’s refining margin swaps:

increase/(decrease)

in equity

2020 2019

rM’000 rM’000

10% increase in refining margin (3,070) (88,750)

10% decrease in refining margin 3,070 88,750