Page 111 - HRC_AR2020

P. 111

HENGYUAN REFINING COMPANY BERHAD I 109

5 fair ValUe MeasUreMents

financial instruments carried at amortised cost

The carrying amounts of financial assets and liabilities measured at amortised cost approximate their respective fair values.

financial instruments carried at fair value

Refining margin swap contracts, forward foreign currency contracts, forward priced commodity contracts, commodity options,

commodity swap contracts and interest rate swap contracts are valued using a valuation technique with market observable

inputs. The most frequently applied valuation techniques include forward pricing model, using present value calculations.

The models incorporate various inputs including the credit quality of counterparties and foreign exchange spot and

forward rates.

fair value hierarchy

The Company measures fair value using the following fair value hierarchy that reflects the significance of the input used in

making the measurements:

Level 1 - quoted prices (unadjusted) in active markets for identical assets or liabilities;

Level 2 - inputs other than quoted prices included within Level 1 that are observable for the asset or liability, either directly

(i.e., as prices) or indirectly (i.e., derived from prices); and

Level 3 - inputs for the asset or liability that are not based on observable market data (i.e., unobservable inputs).

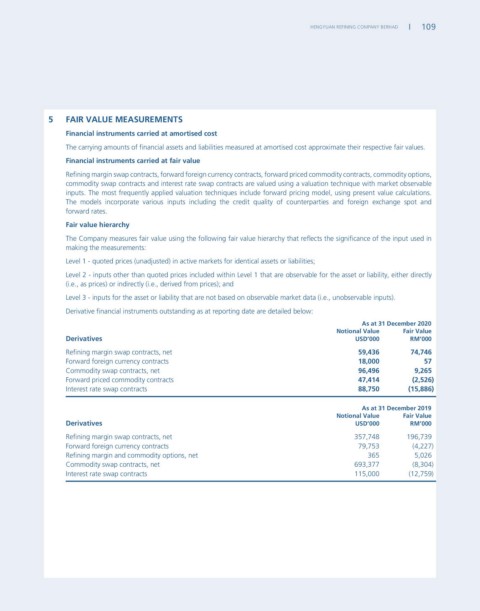

Derivative financial instruments outstanding as at reporting date are detailed below:

as at 31 December 2020

notional Value fair Value

Derivatives UsD’000 rM’000

Refining margin swap contracts, net 59,436 74,746

Forward foreign currency contracts 18,000 57

Commodity swap contracts, net 96,496 9,265

Forward priced commodity contracts 47,414 (2,526)

Interest rate swap contracts 88,750 (15,886)

as at 31 December 2019

notional Value fair Value

Derivatives UsD’000 rM’000

Refining margin swap contracts, net 357,748 196,739

Forward foreign currency contracts 79,753 (4,227)

Refining margin and commodity options, net 365 5,026

Commodity swap contracts, net 693,377 (8,304)

Interest rate swap contracts 115,000 (12,759)