Page 105 - HRC_AR2020

P. 105

HENGYUAN REFINING COMPANY BERHAD I 103

4 financial risK ManaGeMent oBJectiVes anD policies (continued)

(a) Market risk (continued)

(i) foreign currency exchange risk (continued)

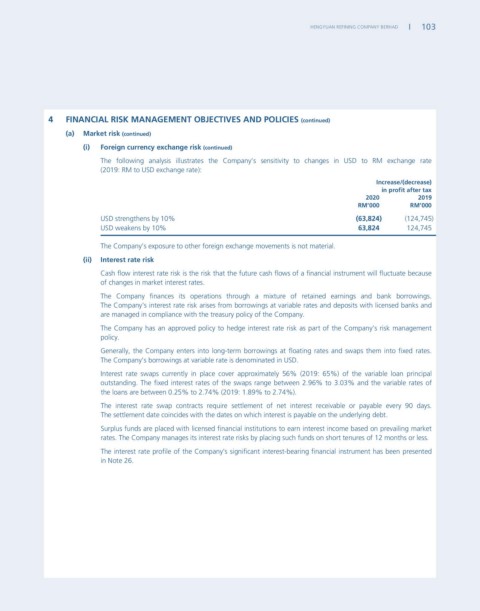

The following analysis illustrates the Company’s sensitivity to changes in USD to RM exchange rate

(2019: RM to USD exchange rate):

increase/(decrease)

in profit after tax

2020 2019

rM’000 rM’000

USD strengthens by 10% (63,824) (124,745)

USD weakens by 10% 63,824 124,745

The Company’s exposure to other foreign exchange movements is not material.

(ii) interest rate risk

Cash flow interest rate risk is the risk that the future cash flows of a financial instrument will fluctuate because

of changes in market interest rates.

The Company finances its operations through a mixture of retained earnings and bank borrowings.

The Company’s interest rate risk arises from borrowings at variable rates and deposits with licensed banks and

are managed in compliance with the treasury policy of the Company.

The Company has an approved policy to hedge interest rate risk as part of the Company’s risk management

policy.

Generally, the Company enters into long-term borrowings at floating rates and swaps them into fixed rates.

The Company’s borrowings at variable rate is denominated in USD.

Interest rate swaps currently in place cover approximately 56% (2019: 65%) of the variable loan principal

outstanding. The fixed interest rates of the swaps range between 2.96% to 3.03% and the variable rates of

the loans are between 0.25% to 2.74% (2019: 1.89% to 2.74%).

The interest rate swap contracts require settlement of net interest receivable or payable every 90 days.

The settlement date coincides with the dates on which interest is payable on the underlying debt.

Surplus funds are placed with licensed financial institutions to earn interest income based on prevailing market

rates. The Company manages its interest rate risks by placing such funds on short tenures of 12 months or less.

The interest rate profile of the Company’s significant interest-bearing financial instrument has been presented

in Note 26.