Page 118 - HRC_AR2020

P. 118

116 I 2020 ANNUAL REPORT I financial reports

NOTES TO THE FINANCIAL STATEMENTS

FOR THE FINANCIAL YEAR ENDED 31 DECEMBER 2020 (CONTINuED)

13 propertY, plant anD eQUipMent (continued)

reversal of impairment in the previous financial year

In financial year ended 31 December 2014, the company recognised an impairment of its plant, machinery and equipment.

The impairment recognised was triggered by the declining trend in refining margins and the announcement by the relevant

regulatory bodies of its intention to implement E4M and Euro 5 compliant fuel by 2019 and 2020 respectively. Assessment

of the asset’s recoverable amount was made, and this resulted in the partial reversal of impairment in the previous

financial years. Management and the Directors had assessed impairment for reversal after taking into consideration the

successful completion of Clean Air Regulation (“CAR”) unit and higher certainty on the progress of the other key regulatory

driven projects, namely Euro 5 Diesel and Hydrogen Generation (“H2GEN”) units. The recoverable amount of the refinery

assets, being defined as a cash-generating-unit, was determined using the FVLCTS method based on management’s

assessment adjusted for market conditions to reflect market participants’ perspective. The FVLCTS is the net present value

of the projected future cashflow derived from the asset discounted at an appropriate discount rate. Refer Note 3(a) for the

key assumptions used.

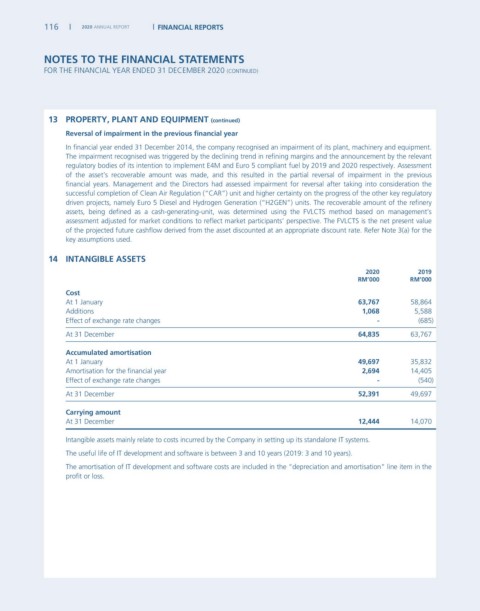

14 intanGiBle assets

2020 2019

rM’000 rM’000

cost

At 1 January 63,767 58,864

Additions 1,068 5,588

Effect of exchange rate changes - (685)

At 31 December 64,835 63,767

accumulated amortisation

At 1 January 49,697 35,832

Amortisation for the financial year 2,694 14,405

Effect of exchange rate changes - (540)

At 31 December 52,391 49,697

carrying amount

At 31 December 12,444 14,070

Intangible assets mainly relate to costs incurred by the Company in setting up its standalone IT systems.

The useful life of IT development and software is between 3 and 10 years (2019: 3 and 10 years).

The amortisation of IT development and software costs are included in the “depreciation and amortisation” line item in the

profit or loss.